1 August 2024, Shafiq Fathullah Shaharuddin

Highlights

- What is E-Invoicing?

- Example e-invoice

- Example non-e-invoice

- Document Under e-Invoice

- E-invoice Mechanism

- E-invoice Workflow

- What is MSME, SME and ME

- Key Component Businesses Need to Know Before E-Invoice Implementation

- E-Invoice Process

- Method of E-Invoice Issuance

- E-Invoice Process (Web Portal / Mobile Apps)

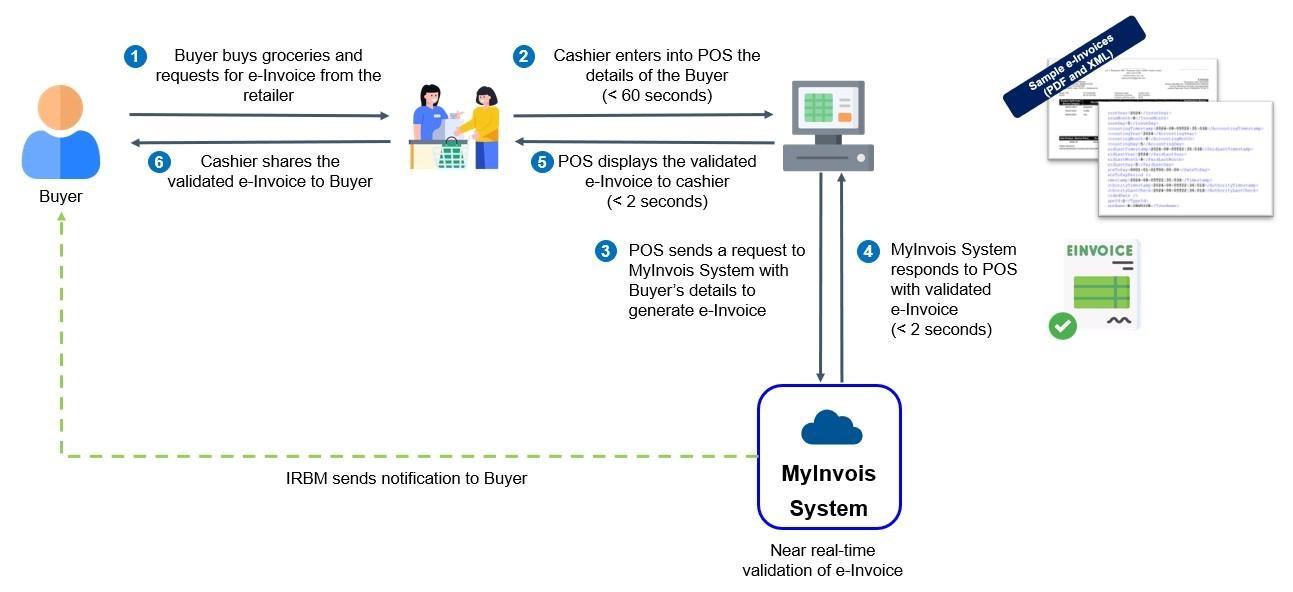

- E-Invoice Process (Point-of-Sales System)

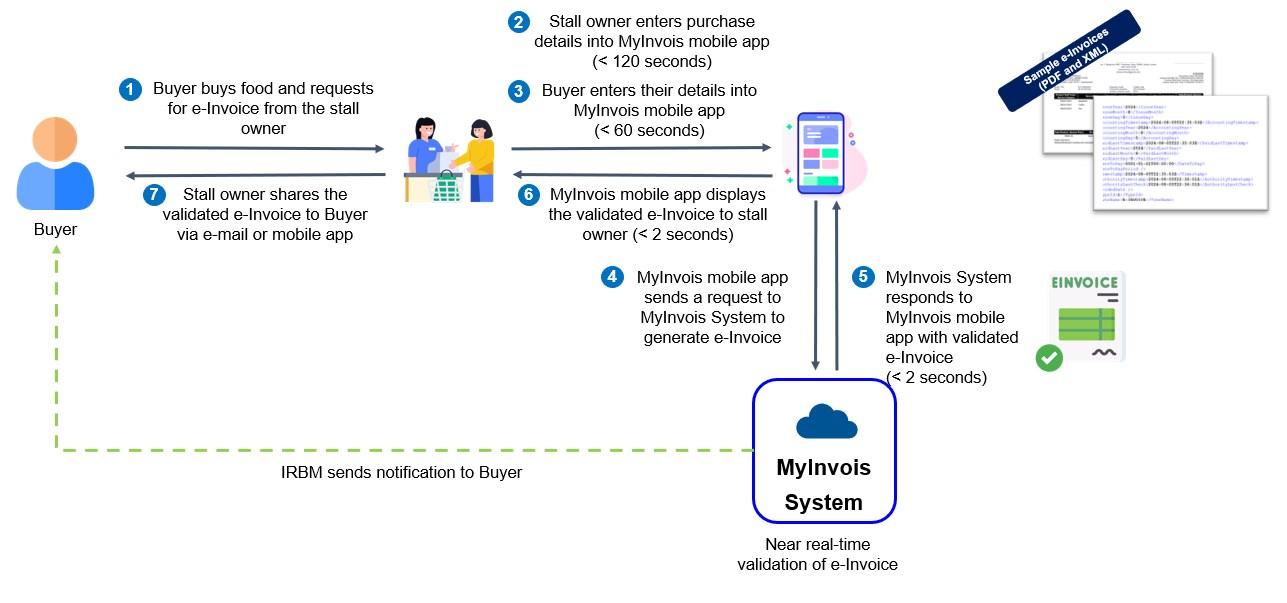

- E-Invoice Process (MyInvoice Mobile Apps)

- Single E-Invoice VS Consolidated E-Invoice

- E-Invoice for Agents, Dealers, Distributors & Affiliates

- MyInvois Portal

What is E-Invoicing?

E-invoicing is the digital representation of transactions between a supplier and buyer, replacing traditional paper or electronic documents such as invoices, credit notes, and debit notes.

Example e-invoice

Example non-e-invoice

Document Under e-Invoice

- Invoice: A commercial document that itemizes and records a transaction between a Supplier and Buyer, including issuance of self-billed e-Invoice to document an expense.

- Credit note: A credit note is issued by Suppliers to correct errors, apply discounts, or account for returns in a previously issued e-Invoice with the purpose of reducing the value of the original e-Invoice. This is used in situations where the reduction of the original e-Invoice does not involve return of money to the Buyer.

- Debit note: A debit note is issued to indicate additional charges on a previously issued e-Invoice.

- Refund note: A refund note e-Invoice is a document issued by a Supplier to confirm the refund of the Buyer’s payment. This is used in situations where there is a return of money to the Buyer.

All taxpayers engaging in commercial activities in Malaysia must issue e-invoices. This includes:

- Individuals, Group and Entities

- Businesses across all industries (trading and services)

- Business-to-business (B2B)

- Business-to-consumer (B2C)

- Business-to-government (B2G)

Exemptions:

- Rulers and related parties

- Government and related government entities

E-invoice Mechanism

- MyInvois Portal:

- Hosted by IRBM

- Accessible to all taxpayers at no cost (Free)

- Available to taxpayers needing to issue a e-invoices where API connection is unavailable

- Application Programming Interface (API):

- Enables direct data transmission between taxpayers’ systems and the MyInvois system

- Requires upfront investment in technology and adjustments to existing systems

- Ideal for large taxpayers or businesses with substantial transaction volumes

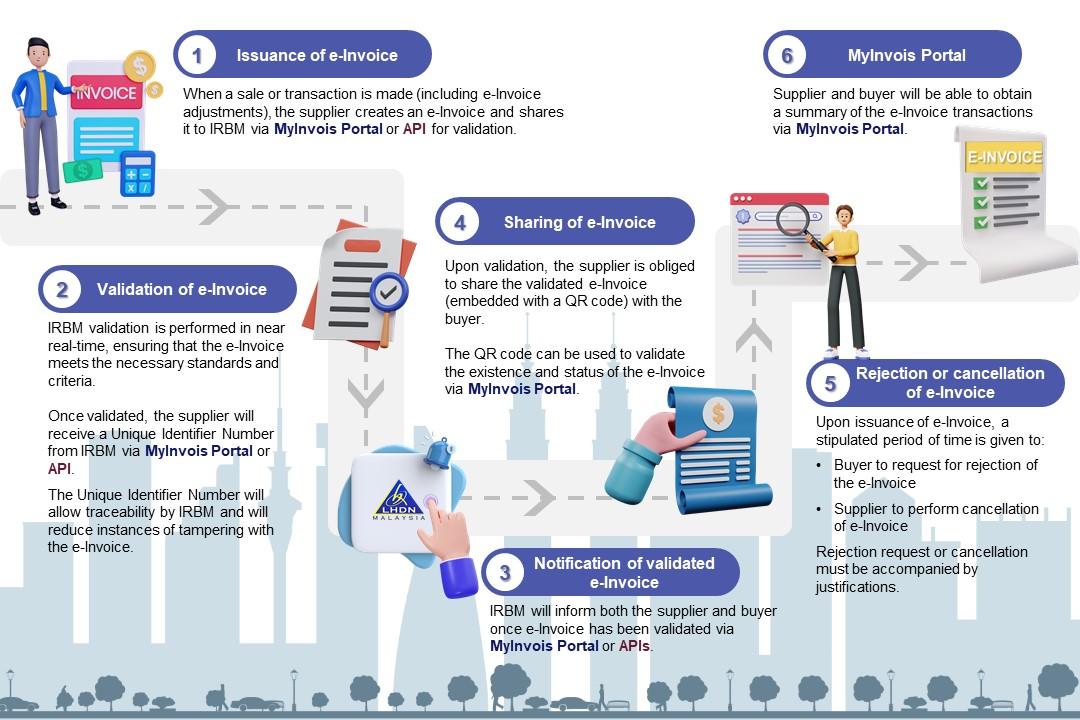

E-Invoice Workflow

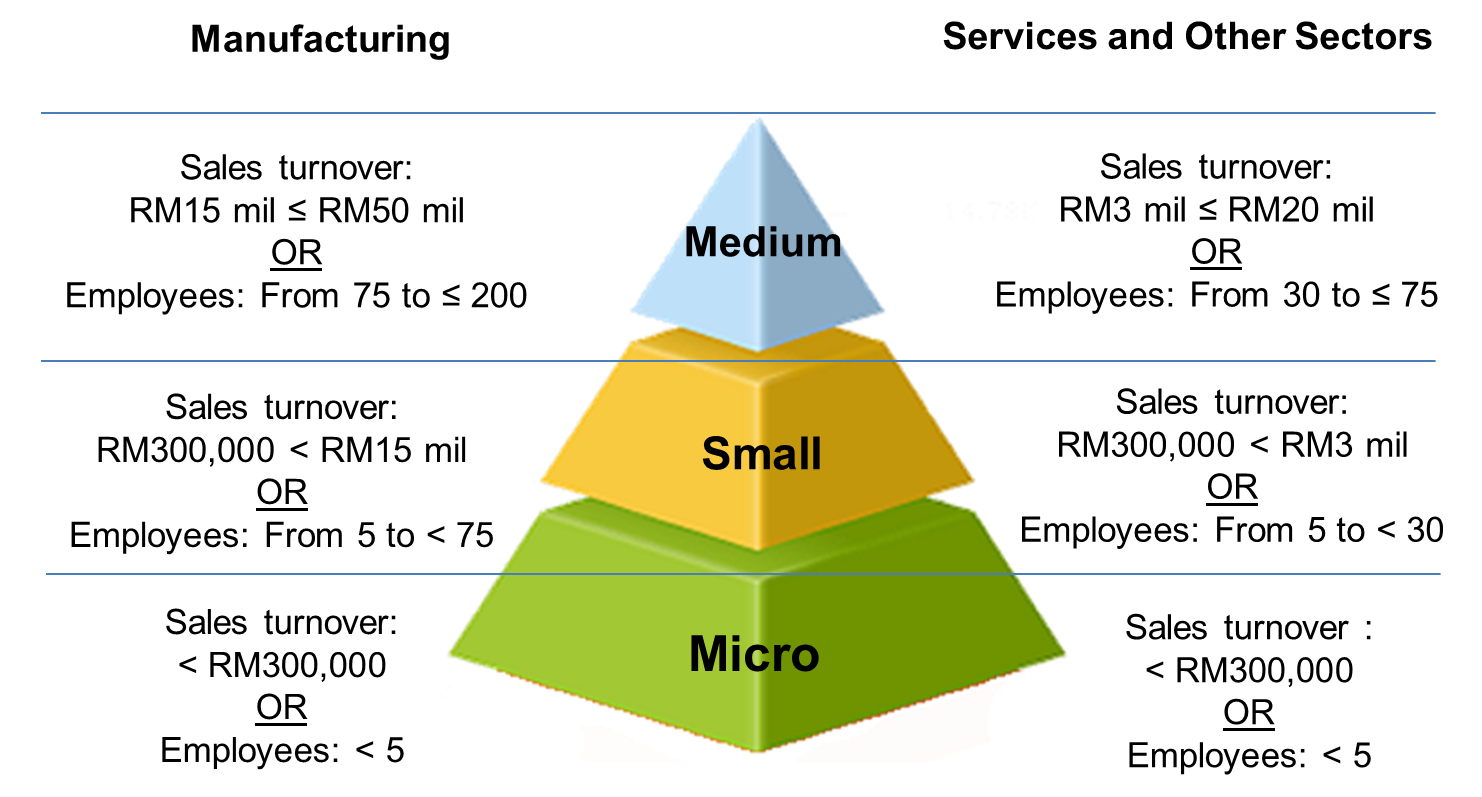

What is MSME, SME and ME

Implementation Timeline

| Targeted Taxpayers | Implementation Date |

|---|---|

| Taxpayers with an annual turnover or revenue of more than RM 100 million | 1 August 2024 |

| Taxpayers with an annual turnover or revenue of more than RM 25 million and up to RM 100 million | 1 January 2025 |

| All taxpayers | 1 July 2025 |

- Taxpayers with audited financial statements: Based on annual turnover or revenue stated in the statement of comprehensive income in the audited financial statements for financial year 2022.

- Taxpayers without audited financial statements: Based on annual revenue reported in the tax return for the year of assessment 2022.

- In the event of a change of accounting year end for financial year 2022, the taxpayer’s turnover or revenue will be pro-rated to a 12-month period for purposes of determining the e-Invoice implementation date.

- Transition Period (01 Aug 2024 – 30 June 2025):

- All other taxpayers can use either normal receipts or validated e-invoices.

- Taxpayers can volunteer to implement e-invoicing earlier.

- New businesses/operations commencing from the year 2023 will implement e-invoicing starting 01 July 2025.

Latest Update by the Inland Revenue Board of Malaysia (Published on 2 July 2024 & 26 July 2024):

- SMEs earning below RM 150,000 annually are exempted from the e-invoice regime.

- MSMEs can issue consolidated e-invoices, combining all sales transactions for each month.

- Traders who develop their own systems or use technology providers, including software packages, will receive tax incentives in the form of Capital Allowance claims effective from the year 2024.

- MSMEs can claim a tax deduction of up to RM 50,000 for consulting fee expenses incurred from the assessment year 2024 to 2027.

- Relaxation of 6 months for mandatory e-invoice implementation for 1 batch taxpayer.

Key Component Businesses Need to Know Before E-Invoice Implementation

- Identify your TIN number.

- Determine your revenue threshold (based on 2022 income).

- Identify your business activities.

- Identify your MSIC code (if necessary)

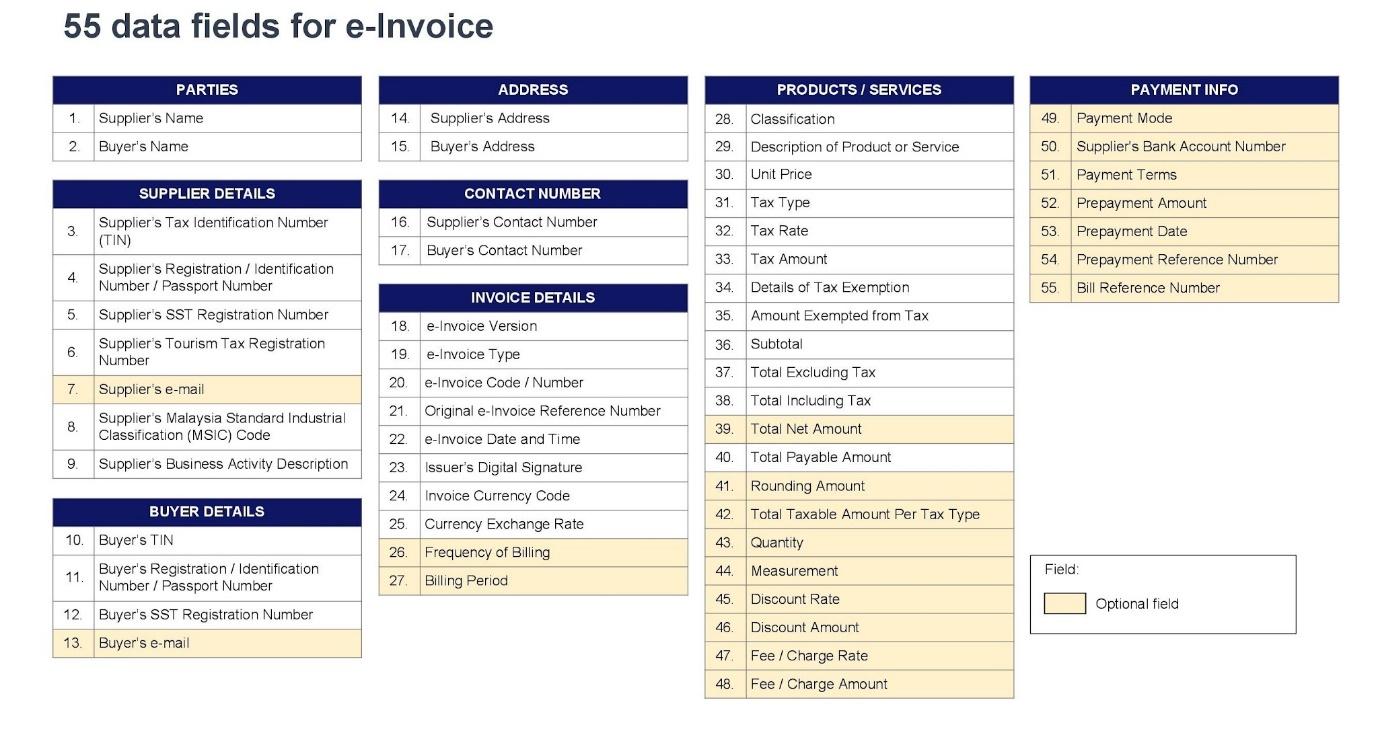

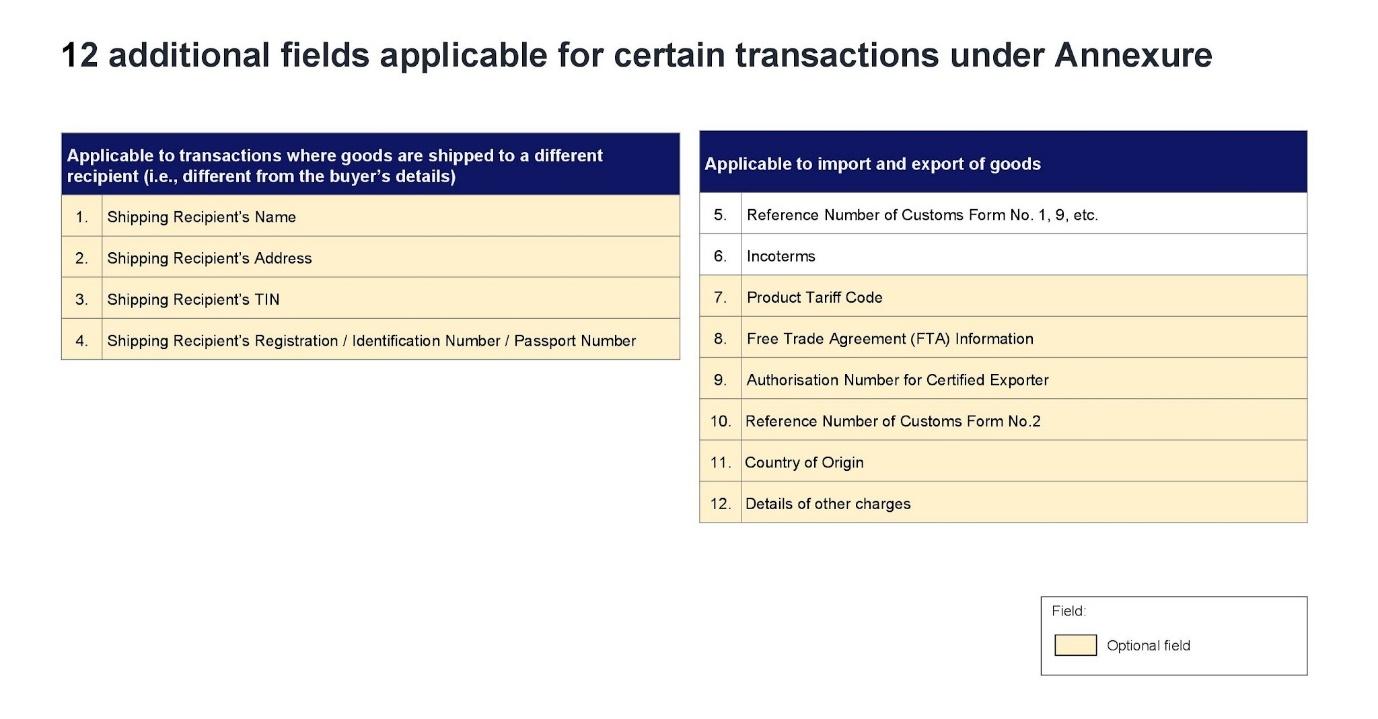

The Number of Data Fields Required For E-Invoice Preparation

- 55 data fields for e-invoice

- 12 additional fields applicable for certain transactions under Annexure

Basic Information Required for E-Invoice (From Buyer)

- Tax Identification Number (TIN Number) (if Applicable)

- Business Registration Number (BRN) / NRIC Number

- SST Registration Number (If Applicable)

- Name of Buyer as per Company Registration, NRIC No, or Passport

- Address

- Phone Number

- Email Address

- MSIC Code (If Applicable)

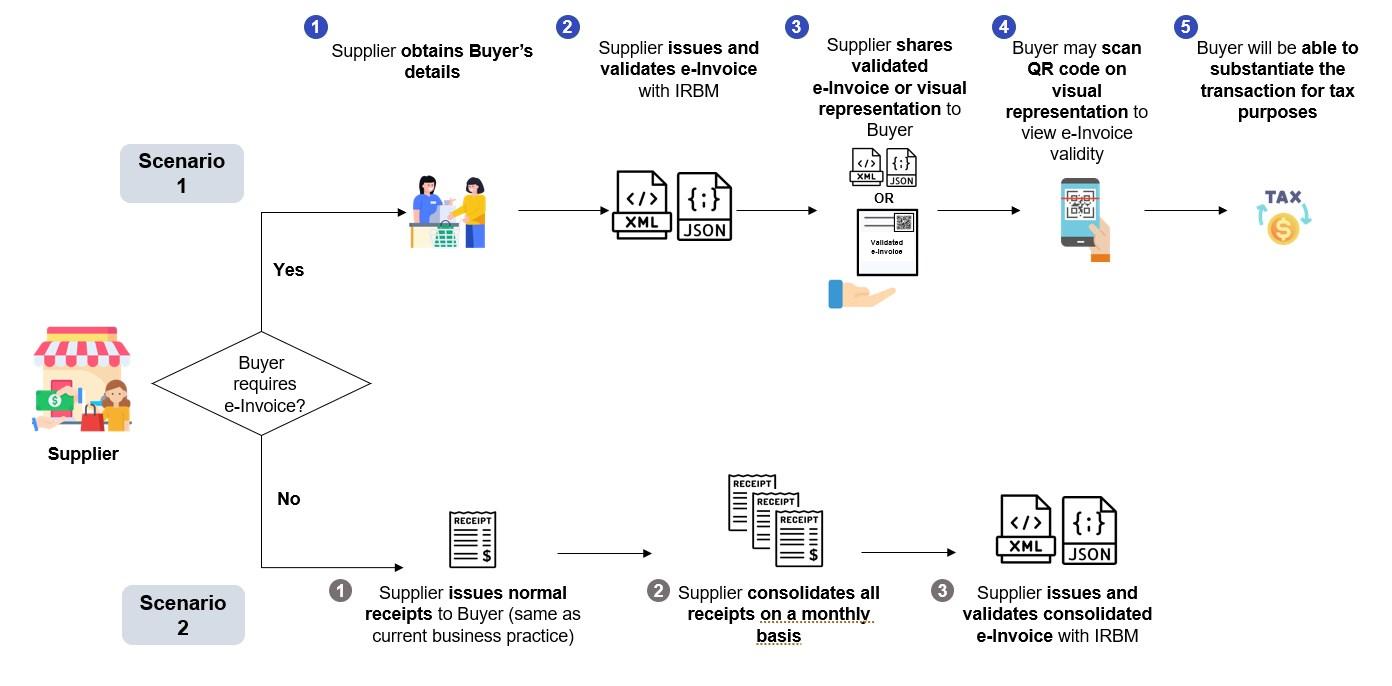

E-Invoice Process

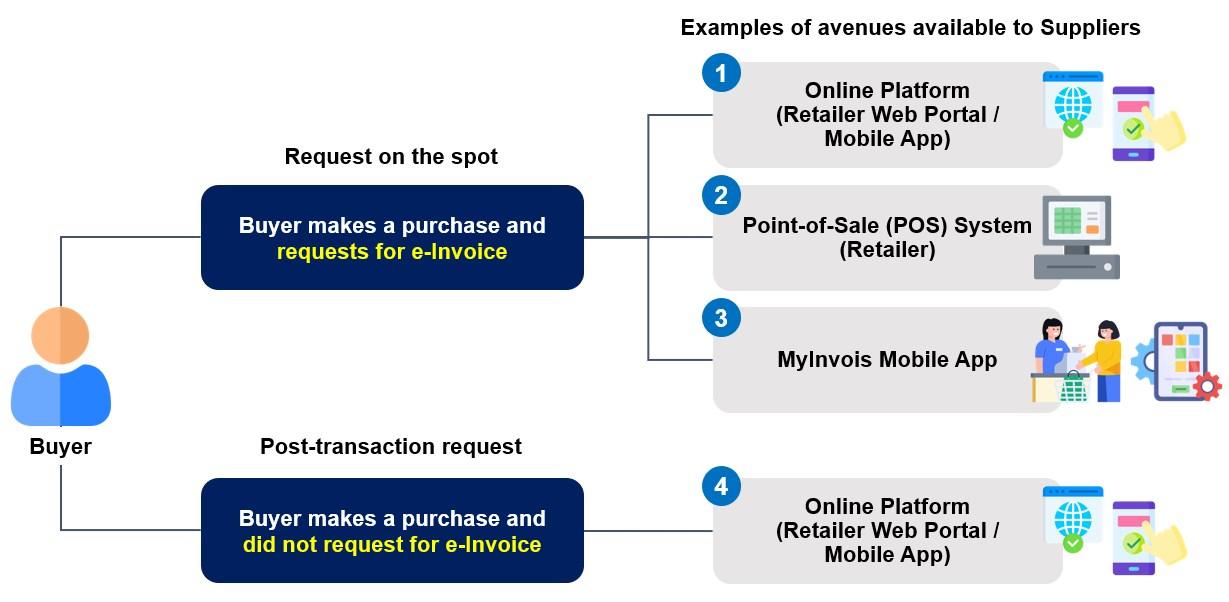

Method of E-Invoice Issuance

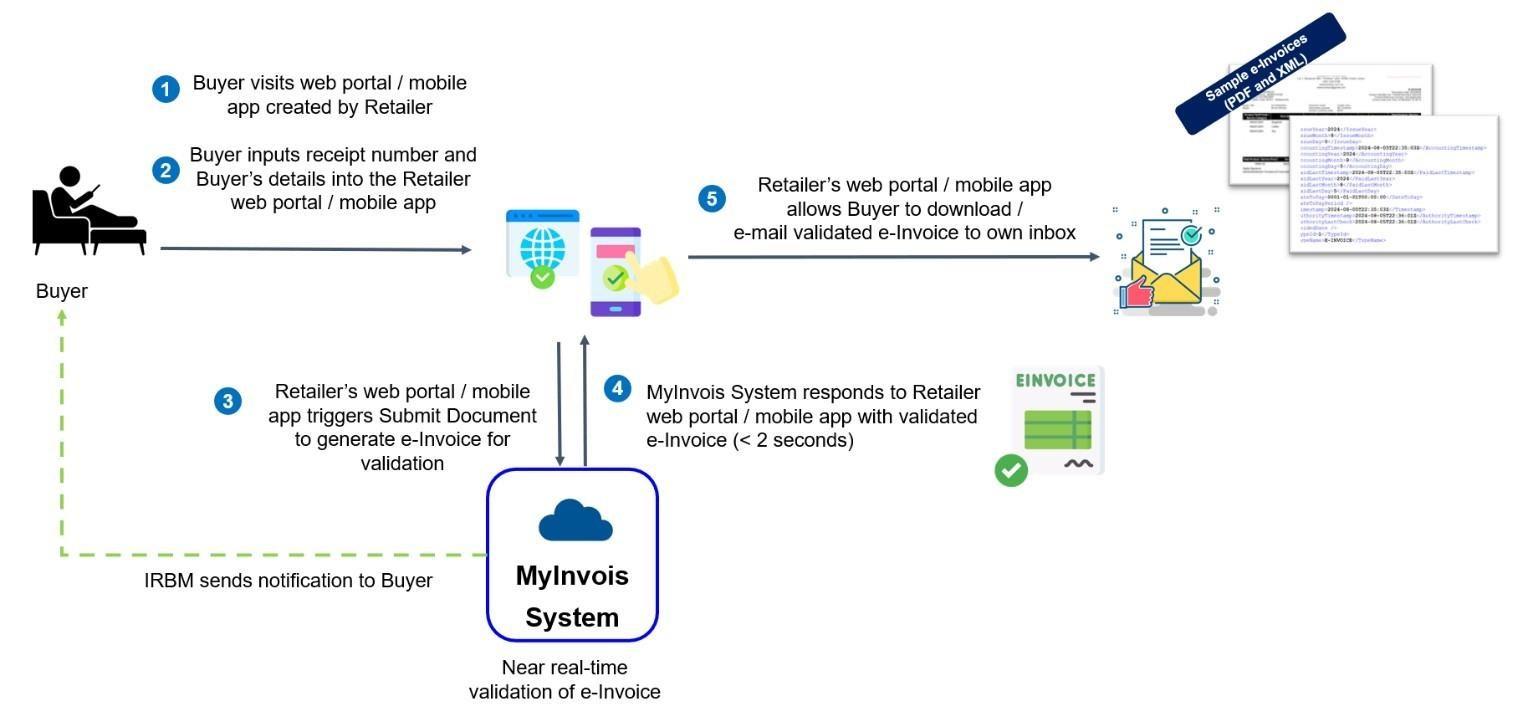

E-Invoice Process (Web Portal / Mobile Apps)

E-Invoice Process (Point-of-Sales System)

E-Invoice Process (MyInvoice Mobile Apps)

Single E-Invoice VS Consolidated E-Invoice

| Single E-Invoice | Consolidated E-Invoice |

|---|---|

| An invoice issued to a customer for a single transaction. | Combines multiple transactions or sales into a single document. |

Example:

Sales for January 2024 from 01.01.2024 to 31.01.2024 can be consolidated into one invoice for e-invoice validation and submission.

(Note: Submissions must be made within 7 days after the month ends)

Activities That Do Not Allow Consolidated E-Invoices

- Automotive

- Aviation

- Luxury goods & jewellery

- Construction

- Wholesalers & retailers of construction materials (e.g., hardware shops)

- Licensed betting and gaming

- Payments to agents/dealers/distributors

Statement / Bills on a Periodic Basis

- Suppliers are required to issue e-Invoice as proof of income and/or proof of expense for items that are shown in the statement / bill.

- In other words, Suppliers are allowed to include the amount owed by Buyers to the Supplier as well as payment / credit to Buyers in the same e-Invoice.

- IRBM allows Suppliers that issue statements / bills on a periodic basis to issue e-Invoice in the format of XML or JSON for IRBM’s validation and convert the validated e-Invoice into visual presentation in the form of statements / bills, to be sent to Buyers.

- Supplier is allowed to create and submit e-Invoice for IRBM’s validation in accordance with their respective issuance frequency (e.g., monthly, bi-monthly, quarterly, bi-annually, annually)

- These industries / sectors include but not limited to:

- Digital / Electronic payment

- Financial services, including banking and financial institutions

- Healthcare

- Insurance

- Stockbroking

- Telecommunications

Rejection and Cancellation of e-invoice

- Once the e-invoice is validated by the LHDN, the seller and buyer are allowed to cancel and reject the e-invoice within the stipulated time of 72 hours, provided they have valid reasons.

- Any amendments to the e-invoice after 72 hours of validation must be made through a credit note, debit note, or refund note.

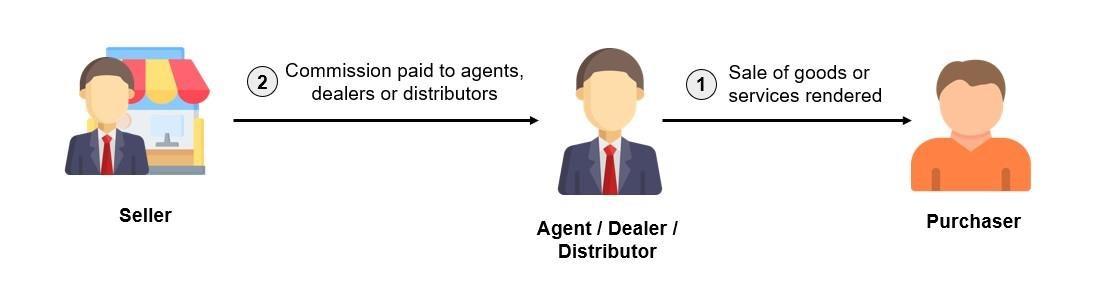

E-Invoice for Agents, Dealers, Distributors & Affiliates

Employers must issue a self-billed e-invoice on behalf of agents, dealers, and distributors to document commission or fee payments.

Example Scenario:

- Foo (Agent) works as a sales agent at AAA Auto Sdn Bhd (Seller).

- Foo is entitled to a 10% commission for every car sold.

- Foo sells a RM 450,000 EV car to Roslan (Buyer).

Steps:

Step 1: AAA Auto Sdn Bhd issues an e-invoice to Roslan (Buyer) (mandatory for the automotive industry).

Step 2: AAA Auto Sdn Bhd issues a self-billed e-invoice to Foo (Agent) for the commission earned.

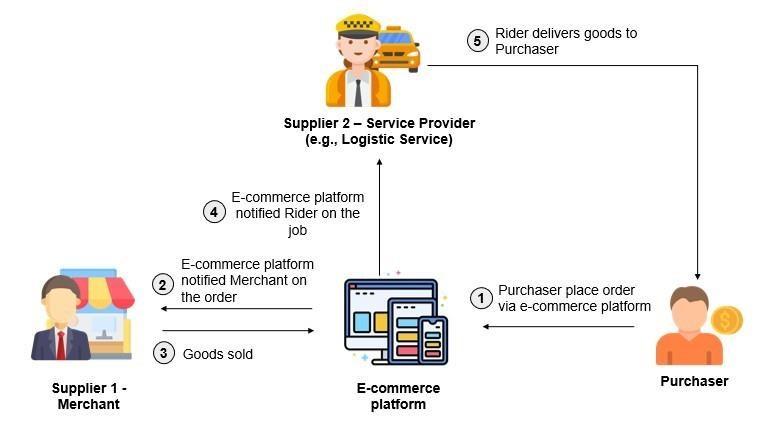

e-Commerce Transactions

- E-commerce transaction means any sale or purchase of goods or services, conducted over any networks by methods specifically designed for the purpose of receiving or placing of orders.

- An e-commerce transaction can be between various parties, such as enterprises, households, individuals, governments, and other public or private organizations.

- Upon implementation of e-Invoice, e-commerce platform providers are responsible to assume the role of Supplier in facilitating the issuance of:

- E-Invoice (upon Purchaser’s request); or

- Receipt (if no e-Invoice is requested by the Purchaser) to the Purchaser for the transaction.

Cross-Border Transactions

Cross-border transactions involve goods sold or services provided by a foreign seller to a Malaysian buyer or vice versa.

| Imported Goods and Services | Exported Goods and Services |

|---|---|

| Foreign sellers are not required to implement Malaysia’s e-invoice. | Malaysian sellers must implement Malaysia’s e-invoice. |

| Malaysia-based buyers must issue self-billed e-invoices. | A generic TIN number is provided for foreign buyers. If not available, the local seller will use the general TIN number. |

Self-Billed e-invoice

- When a sale or transaction is concluded, an e-Invoice is issued by Supplier to recognize income of the Supplier (proof of income) and as a record for purchases made / spending by Buyer (proof of expense).

- However, there are certain circumstances where another party (other than the Supplier) (Buyer) will be required to issue a self-billed e-Invoice.

- For e-Invoice purposes, Buyer shall issue self-billed e-Invoices for the following transactions:

- Payment to agents, dealers, distributors, etc.

- Goods sold or services rendered by foreign suppliers

- Profit distribution (e.g., dividend distribution)

- Electronic commerce (“e-commerce”)

- Pay-out to all betting and gaming winners

- Transactions with individuals (who are not conducting a business)

- Interest payment, except:

- Businesses (e.g., financial institutions, etc.) that charge interest to public at large (regardless of whether they are businesses or individuals);

- Interest payment made by employee to employer; and Interest payment made by foreign payor to Malaysian taxpayers.

- Claim, compensation or benefit payments from the insurance business of an insurer

Employee’s Benefits / Claims & Reimbursement

- Employees are required to request a validated e-invoice from the supplier for claiming purposes (whenever possible).

- The e-invoice can be issued any the situation as follows:

- E-invoice issued under the employee’s name

- Using the existing document issued by the supplier

- In the situation when the bills/invoice issued by the foreign supplier:

- Employee can use the existing bills/invoice issued by the foreign supplier

- No requirement for the employee to issue self-billed e-invoice

General Tax Identification Number (TIN)

| General TIN Number | Situation of Usage |

|---|---|

| “EI00000000010” as General Public’s TIN | – Individual’s (i.e., Supplier, Buyer, Shipping Recipient) TIN in the e-Invoice for Malaysian individual where the individual only provides MyKad / MyTentera identification number – Buyer’s TIN in the consolidated e-Invoice – Supplier’s TIN in the consolidated self-billed e-Invoice |

| “EI00000000020” as Foreign Buyer’s / Foreign Shipping Recipient’s TIN | – Buyer’s TIN in the e-Invoice for non-Malaysian individual where the individual buyer only provides passport number / MyPR / MyKAS identification number – Buyer’s TIN for export transactions where foreign buyer’s TIN is not available or not provided – Shipping Recipient’s TIN for where foreign shipping recipient’s TIN is not available or not provided |

| “EI00000000030” as Foreign Supplier’s TIN | – Supplier’s TIN in the e-Invoice for non-Malaysian individual where the individual supplier only provides passport number/ MyPR/ MyKAS identification number (applicable for self-billed e-Invoice) – Supplier’s TIN for import transactions where foreign supplier’s TIN is not available or not provided (applicable for self-billed e-Invoice) |

| “EI00000000040” as Buyer’s TIN | – Buyer’s TIN for transactions involving the following persons: > Government > State government and state authority Government authority > Local authority > Statutory authority and statutory body > Exempt institutions that are not assigned with TIN |

MyInvois Portal

The MyInvois portal is a platform developed by the LHDN to facilitate the implementation of the electronic invoicing (e-invoicing) system in Malaysia. This portal aims to streamline and digitize the invoicing process for businesses, enabling them to generate, send, receive, and store invoices electronically.

Key Features included

- E-invoice Generation and Submission: Businesses can create and submit invoices electronically through the portal.

- Compliance: Ensures that invoices meet the regulatory requirements set by the LHDN.

- Data Security: Implements measures to secure invoicing data and protect sensitive business information.

- Integration: Allows integration with existing accounting and invoicing software used by businesses.

- Real-time Processing: Facilitates real-time processing and validation of invoices.

- Record Keeping: Provides a digital repository for storing and accessing historical invoices.

First Time Login

- For the application of ‘Company Director’ role and the appointment of ‘Company Representative’ role by the Director.

- First Time Login must be login from the Mytax Portal of the appointed Company Director.

- Applications for the role of ‘Company Director’ for sole proprietorship businesses and Labuan Entities are not yet available.

- Appointments of ‘Company Representative’ are also required through Company Director MyTax Portal.

Impact of E-Invoice Implementation

| Positive Impacts | Challenges |

|---|---|

| All business transaction reporting is expected to be digitized | Initial costs related to software adoption and training. |

| Enhanced tax compliance and collection | Ensuring the security of digital transactions and safeguarding sensitive information is crucial. |

| Increased operational efficiency | Integration of e-invoicing systems with existing accounting and ERP systems may require technical adjustments. |

| Improved transparency and accountability |

What to Expect from E-Invoice Implementation:

- The invoice is final once created and verified by LHDN. No edits are allowed after creation.

- Adjustments must be made through additional debit notes, credit notes, or refund notes.

- No more backdated or post-dated transactions.

- Manual invoices (e.g., Excel/Word) are no longer permitted.

Failing to issue an e-invoice will be penalized under section 120(1) of the Income Tax Act, 1967, with a minimum penalty of RM 200 and a maximum of RM 20,000-, or 6-months imprisonment, or both.